Introduction

Blockchain technology is experiencing rapid growth, boasting a Compound Annual Growth Rate (CAGR) of 85.9%. By 2030, its market value is anticipated to surge to approximately $1432 billion. This blog post, tailored for E-Startups Kenya, explores blockchain’s fundamentals, its benefits and drawbacks, and its operational mechanics.

What is Blockchain?

Blockchain is essentially a network of interconnected blocks that securely store data across multiple points, allowing for easy traceability of its origin. It serves as a decentralized database or ledger, accessible across various computer network nodes. This technology ensures the integrity and security of data without needing a third-party intermediary.

Each block can hold data like transaction details, times, and methods, as desired by the user. When a block reaches its capacity limit, it’s sealed and linked to the preceding block, thus forming a chain of data blocks. This data structure differs from traditional databases by not storing data in tables but rather in blocks that are securely linked together.

Advantages of Blockchain

Blockchain technology offers numerous benefits:

- Open Source: It is open to everyone, requiring no permission to participate in the distributed network.

- Authenticity and Security: With decentralized data storage, the authenticity of information can be verified through methods like zero-knowledge proofs without compromising data privacy.

- Permanence: The decentralized nature of blockchain makes the data virtually immutable and secure across multiple reliable nodes.

- Efficiency: By eliminating intermediaries, blockchain transactions become quicker and more efficient.

Disadvantages of Blockchain

Despite its benefits, blockchain also has some limitations:

- Scalability: The fixed size of blockchain blocks limits the number of transactions that can be processed simultaneously.

- Speed: The process of adding new blocks, which involves solving complex cryptographic tasks, can be slow and inefficient for large-scale applications.

- Legal and Regulatory Challenges: Various legal constraints and environmental concerns in different countries can affect blockchain implementation.

Benefits of Blockchain

- Enhanced Security: The end-to-end encryption and tamper-proof nature of transactions secure data against unauthorized access and fraud.

- Transparency: With a distributed ledger, all permitted participants have access to the same information at the same time, ensuring full transparency.

- Traceability: Every transaction on a blockchain can be easily traced, improving the accountability and integrity of the supply chain.

- Automation: Smart contracts on blockchain automate transactions, further enhancing efficiency and reliability.

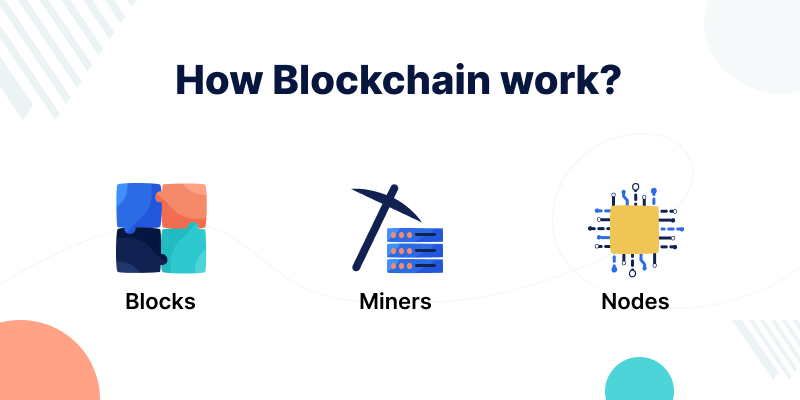

How Does Blockchain Work?

Blockchain functions through several core components:

- Blocks: Each block stores data and is linked to the chain once filled, each having a unique cryptographic signature.

- Miners: These are entities or processes that validate new transactions and record them into the blockchain.

- Nodes: Every part of the blockchain network that maintains copies of the ledger and ensures its operation.

How Can E-Startups Kenya Assist You?

E-Startups Kenya stands at the forefront of eCommerce innovation in Nairobi, offering cutting-edge solutions for B2B and B2C marketplaces. Our expertise extends to facilitating secure digital transactions through blockchain technology, enhancing both transparency and efficiency for our clients.

Conclusion

Blockchain is a dynamic and evolving technology that promises to transform data management and transaction processes. With its robust security features and efficiency, it is set to play a crucial role in the future of digital transactions, particularly in innovative markets like Kenya. E-Startups Kenya is excited to be part of this transformative journey, offering our customers and partners the best in technology solutions.